All Categories

Featured

Table of Contents

That typically makes them a much more inexpensive choice for life insurance policy protection. Some term policies may not maintain the premium and fatality benefit the very same gradually. Level premium term life insurance. You don't wish to erroneously assume you're acquiring degree term coverage and after that have your survivor benefit change later on. Lots of individuals get life insurance policy coverage to help financially shield their loved ones in instance of their unexpected death.

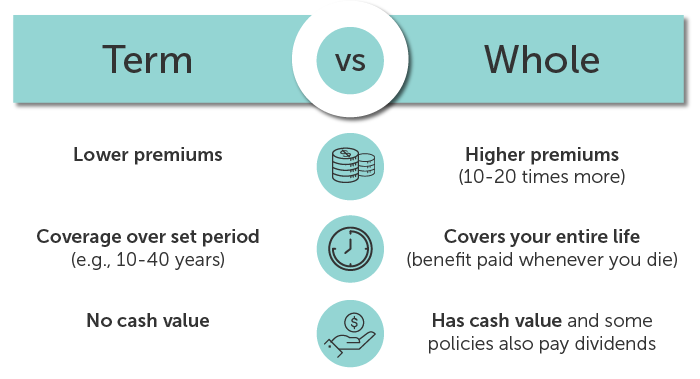

Or you may have the alternative to transform your existing term insurance coverage right into a long-term plan that lasts the rest of your life. Different life insurance policies have prospective advantages and drawbacks, so it's essential to understand each before you choose to acquire a plan. There are a number of benefits of term life insurance policy, making it a preferred selection for protection.

As long as you pay the premium, your recipients will receive the survivor benefit if you die while covered. That claimed, it is essential to note that the majority of plans are contestable for 2 years which indicates protection could be retracted on fatality, should a misstatement be located in the application. Plans that are not contestable frequently have a rated survivor benefit.

What is Joint Term Life Insurance? Your Guide to the Basics?

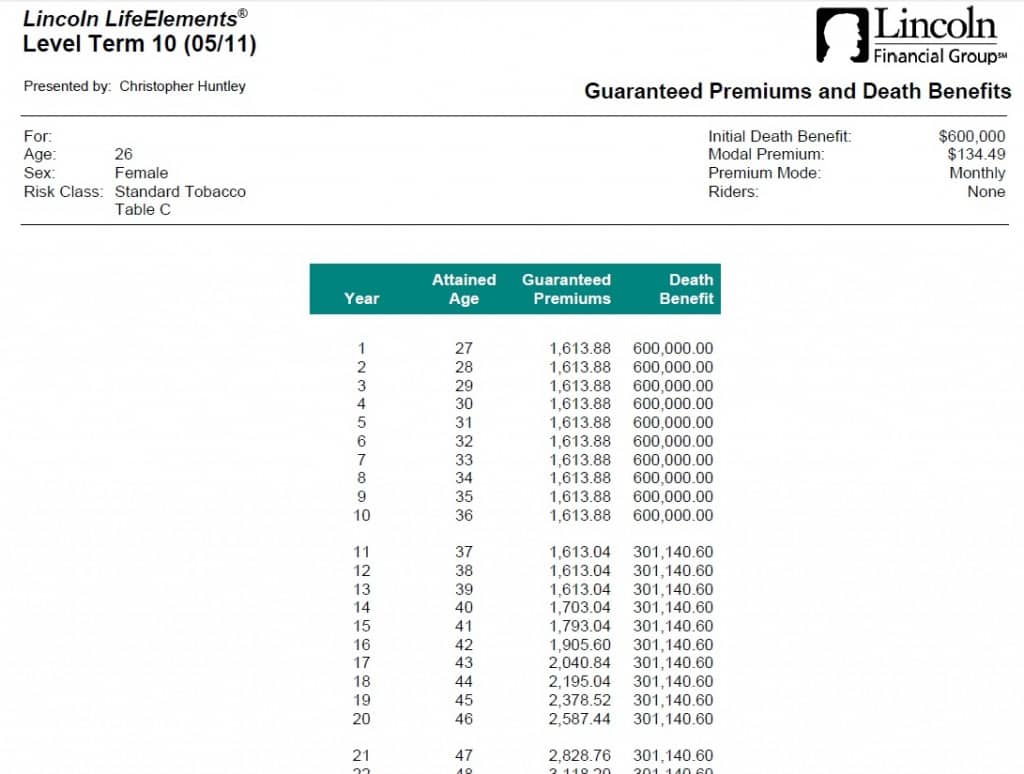

Premiums are usually reduced than whole life plans. With a level term policy, you can pick your coverage amount and the plan length. You're not secured right into an agreement for the rest of your life. Throughout your policy, you never have to bother with the costs or fatality benefit amounts altering.

And you can't squander your plan during its term, so you won't obtain any kind of financial benefit from your past protection. Just like various other sorts of life insurance coverage, the expense of a level term policy depends upon your age, insurance coverage needs, employment, way of living and health and wellness. Typically, you'll discover more inexpensive protection if you're younger, healthier and much less dangerous to insure.

Considering that degree term premiums remain the same for the duration of coverage, you'll know precisely just how much you'll pay each time. Level term protection additionally has some versatility, permitting you to personalize your plan with additional features.

What Is Direct Term Life Insurance Explained

You might have to meet details problems and certifications for your insurance company to enact this biker. There also can be an age or time restriction on the coverage.

The death advantage is normally smaller, and coverage generally lasts until your child turns 18 or 25. This rider may be an extra cost-efficient means to aid ensure your kids are covered as cyclists can frequently cover multiple dependents at the same time. Once your kid ages out of this protection, it may be possible to transform the rider right into a new policy.

When contrasting term versus irreversible life insurance policy, it's vital to bear in mind there are a couple of different types. One of the most usual kind of irreversible life insurance policy is whole life insurance, but it has some essential differences compared to degree term protection. Direct term life insurance meaning. Below's a standard summary of what to consider when contrasting term vs.

Entire life insurance policy lasts forever, while term protection lasts for a details duration. The costs for term life insurance coverage are usually less than entire life coverage. With both, the premiums stay the same for the duration of the policy. Entire life insurance has a money worth component, where a section of the costs may grow tax-deferred for future requirements.

One of the major functions of level term insurance coverage is that your premiums and your death benefit do not change. You might have insurance coverage that begins with a death benefit of $10,000, which can cover a home mortgage, and then each year, the death benefit will lower by a set amount or percentage.

Due to this, it's usually a more budget friendly type of degree term insurance coverage., yet it might not be enough life insurance for your demands.

What is Term Life Insurance With Level Premiums? Important Insights?

After deciding on a plan, complete the application. If you're approved, sign the documents and pay your first premium.

You may want to upgrade your recipient details if you've had any considerable life changes, such as a marital relationship, birth or divorce. Life insurance policy can occasionally feel complicated.

No, level term life insurance policy doesn't have money worth. Some life insurance policy policies have a financial investment feature that enables you to build cash value with time. A part of your premium repayments is set apart and can gain interest in time, which grows tax-deferred during the life of your insurance coverage.

You have some choices if you still desire some life insurance policy protection. You can: If you're 65 and your coverage has run out, for instance, you might desire to buy a brand-new 10-year degree term life insurance coverage plan.

What is What Is Level Term Life Insurance? Learn the Basics?

You may be able to convert your term coverage into an entire life plan that will last for the rest of your life. Lots of sorts of level term policies are exchangeable. That means, at the end of your protection, you can convert some or all of your plan to entire life protection.

A level premium term life insurance policy plan lets you adhere to your budget plan while you aid shield your household. Unlike some stepped price strategies that increases every year with your age, this sort of term strategy provides rates that stay the very same for the period you pick, even as you grow older or your health and wellness adjustments.

Find out more about the Life insurance policy options available to you as an AICPA participant (Joint term life insurance). ___ Aon Insurance Coverage Providers is the trademark name for the broker agent and program management procedures of Fondness Insurance coverage Services, Inc. (TX 13695) (AR 100106022); in CA & MN, AIS Fondness Insurance Coverage Firm, Inc. (CA 0795465); in Alright, AIS Affinity Insurance Coverage Services Inc.; in CA, Aon Fondness Insurance Providers, Inc .

{kind=link}

Latest Posts

Funeral Expense Life Insurance

Life Insurance Or Funeral Plan

Aarp Burial Insurance Seniors